With a CMA review under way, and fuel prices continuing rise to record levels, Tom Hatton, head of Product Management at fuel pricing software specialist Kalibrate, defends fuel retailers

Retailers are being unfairly blamed for fuel prices skyrocketing and while there are reports of individual sites increasing prices excessively, this is absolutely the exception and not the rule.

The UK fuel market has some interesting characteristics – approximately 50% of fuel is sold at a particularly low margin by supermarkets (to drive store footfall), and up to 66% of forecourts in the UK are owned by independents. This means that the UK has a very competitive fuel retail market with conditions that ultimately benefit the consumer, and therefore if trading conditions were to get harder for retailers it’s likely only going to impact consumers in the long run.

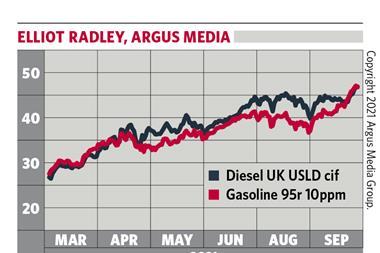

Fuel retailers are facing major disruptions to their businesses. Demand for fuel is extremely volatile and generally declining, operating costs are increasing, and wholesale fuel costs are climbing at previously unseen levels. In recent years, many fuel retailers reimagined their businesses during the pandemic by improving their convenience offerings and subsequently taking on higher operating costs. They are therefore now facing more acute issues than they did even in 2008 – when fuel prices last climbed so sharply – as the global economy did not experience such high rates of inflation and a subsequent cost-of-living crisis.

If a sizeable number of the independents were to go out of business, this would undoubtedly negatively affect consumers both in provision of fuel and market dynamics at the retail end of the supply chain. The bottom line is that fuel is not expensive due to retailers’ pricing tactics, rather fuel is currently expensive for two driving factors: the tax structure (accounting for 46% of the price) and the formulaic nature of oil pricing (also accounting for 46% of the price).

Unfortunately fuel prices could continue to rise over the coming months, and for there to be any improvement to consumer conditions, the most immediate and impactful lever to pull would be to review the tax structures (particularly VAT on fuel) and not retailers’ margins.

No comments yet