Given the petrol filling station sector comprises everything from single-site operators to multi-million-pound corporations, it’s little wonder there are almost as many perspectives about as there are forecourts. But at a recent business lunch that gathered a cross-section of operators together, identifiable themes emerged as conversations progressed.

Among the forecourt operators in attendance were representatives from Ascona, Midland Motor Fuel, Rondel Trading and Sterling Petroleum, along with legal advisors from Winckworth Sherwood, and commercial property experts Christie & Co which hosted the event.

The EV charging landscape

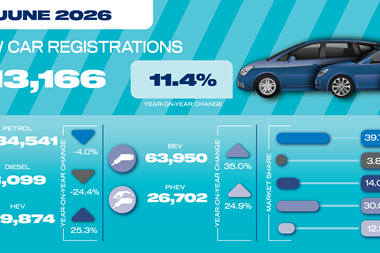

The first item on the agenda was electrification and the ongoing challenge of EV charging infrastructure. While it is understandable that petrol retailers are likely to be sceptical of the push towards EVs, some of the details to be shared were noteworthy, to say the least.

One Midlands-based operator relayed that he had been quoted around £700,000 for the installation of an electrical substation that would be essential for EV charging to be added to one of his sites. And while substations can bring some investment from nearby businesses tapping into them, this significant figure was juxtaposed by another operator who shared that a chargepoint at one of his forecourts had brought in just £60 of revenue one month.

There was also a pointed silence when Steve Rodell from Christie & Co asked the room if anyone could report making a margin on charging.

Despite this, local councils are demanding EV chargers feature in plans when permissions for forecourt construction or refurbishment are submitted, though given local grid capacities can preclude this from becoming a reality, this mandate was spoken of as often being a “tick box” requirement.

It’s not just national and local authorities who are pushing for electrification, though: one operator who had recently applied for financing told the room that banks are increasingly asking firms to demonstrate their net-zero credentials when asking for business loans, with chargepoints high on the list of questions.

To balance this, Rodell pointed out that there are strategically located EV charging hubs which can make significant profit due to being on routes with high traffic flows, or close to dense areas of population where charging at home is difficult or impossible for a high proportion of residents.

Rodell was optimistic for the sector and said he is confident there won’t be need for concern about traditional fuel retailing in general until 2035 at the earliest, and probably well beyond. One operator echoed this, sharing that his multi-site firm is also optimistic for the industry, which can expect to see strong trading for at least 10, if not 15 years. The operator also shared that land is key when looking for acquisitions, and firms should consider larger sites which provide greater scope for diversification options that offer futureproofing.

Shop and social trends

Here, the conversation turned to the potentially declining popularity of Dubai chocolate and micro-USB leads, and the volatile nature of social-media trends and technology, which can leave firms with unsold stock if the wind changes.

This was countered by the relative security of investing in seasonal products, particularly affordable bottled water during the summer months.

Make-up and perfume were being trialled by some operators, according to Christie & Co, with Rodell also saying his firm had recently been asked to value a shop where social media alone was generating weekly revenue of £10,000. Operators agreed that it was vital to understand the localised nature of social media and use it to target those in close proximity to businesses, rather than creating generalised content.

A Winckworth Sherwood representative, meanwhile, reminded those gathered that the forthcoming Tobacco and Vapes Bill will require retailers to obtain a new, separate licence if they want to continue selling these products.

Food, food and more food?

While food-to-go was accepted as an essential aspect of modern forecourt retailing, there was some debate about how best to approach this. Some food-to-go machines were performing better than others, while it was generally accepted that there is a limit to how many offerings one forecourt can play host to.

There was also significant consideration given to franchise food outlets. If a site has strong footfall and shifts several million litres a year, is there really the need for an established brand to pull people in?

One operator thought not, explaining that rather than invite a big fast-food name to join his business he had developed his own on-site café, which was showing strong margins and selling 120 coffees a day, the latter being profitable despite being around a third cheaper than the black gold sold by established coffee chains.

Crime and communities

There was a general acceptance that with police resources unable to sufficiently manage crime, forecourt operators themselves could step up to the plate as this is both good for business, and the right thing to do for surrounding communities.

One operator revealed that his site operates a knife-amnesty box, with staff being completely non-judgemental when someone gives up a blade, while also sharing that they offer free coffee and unlimited parking to police officers, and the businesses’ CCTV systems had been instrumental in helping bring at least half a dozen offenders to justice.

Refreshing pumps, expanding shops, valeting and advertising

‘What next?’ is an evergreen question in retailing, and while there was a general acceptance that expanding forecourt portfolios is seen as a no-brainer at present, there was also recognition that the sector had changed so significantly in recent years that consolidation of existing assets was sometimes the name of the game.

So rather than install another ice-cream machine or car-mat cleaner, operators could instead consider upgrading their pumps and expanding their shops, as both these endeavours can help attract customers. The former reduces maintenance downtime and helps keep a site looking modern, while the latter improves a forecourt’s ‘destination’ pull.

With valeting an established element of forecourt diversification, granular elements of this topic were covered. WashTec systems were spoken of favourably, while Christie & Co revealed advertising firms are increasingly recognising that they can reach audiences in the millions by putting screens on forecourts, especially at points with high dwell times, such as valeting areas.

As the forecourt sector navigates shifting regulations, rising operational costs and changing consumer habits, one thing is clear: adaptability, local insight, and bold investments in infrastructure and customer experience will define the winners of the next decade.