It was only a few days ago that the head of a major chargepoint firm warned that companies in his sector are “running out of money”, and the recent collapse of one firm, together with the acquisition of another, indicates that assessment was valid.

Be.EV’s chief executive, Asif Ghafoor, whom Forecourt Trader has previously interviewed at length, also told The Guardian last Saturday the chargepoint sector was “a very crowded space” with “too many operators”, and that “numerous” firms had approached his company looking for a buyer. “These businesses are going to come together”, he added.

Ghafoor may have been hinting of what was to come, as it has now been revealed that Be.EV has bought the public charging network previously operated by Mer, a Norwegian firm that will now focus only on fleet charging in the UK.

Trojan collapse

Earlier in the week in a separate announcement it was revealed that Aberdeen-based Trojan Energy, which specialises in pavement chargers customers plug a ‘lance’ into, had entered administration, having failed to attract further investment despite winning council contracts to install chargepoints. The firm had received £28m of cash from the government-backed Scottish National Investment Bank, and its assets have been bought by rival firm Connected Kerb, securing 60 jobs.

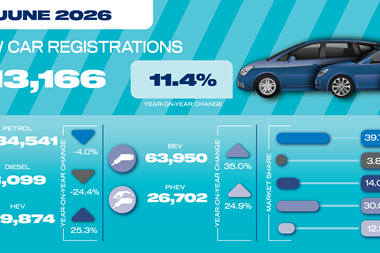

While sales of electric cars are often said to be stymied by a lack of chargepoint infrastructure amounting to chicken-and-egg paradigm, around 90% of EV buyers have the ability to charge their cars at home, leaving a small customer base for commercial firms to chase.

The result is that while government cash, by way of schemes such as the £400m Local Electric Vehicle Infrastructure fund, continues to flow to chargepoint operators as they expand, operating profits can be far harder to come by.

An industry in which loss is the norm

Despite its recent acquisition of Mer, Be.EV’s parent company, Induna Infrastructure, lost £13.3m in 2024, though the firm secured a £55m debt facility from NatWest and German bank KfW in the same year.

Losses in the chargepoint sector are the rule rather than the exception, though. Connected Kerb, buyers of Trojan’s assets, lost £15.7m in 2024. Over the same period Fastned’s UK arm lost £6.2m, Osprey Charging lost £6.1m, Blink Charging lost £5.4m, and Char.gy lost £10.8m in FY 2024/25. Gridserve lost over £80m in the last financial year, while rival firm Instavolt lost £8.5m in 2025, an improvement on the previous year, when it lost £15.6m.

Even oil majors, not known for their lack of profitability, aren’t immune to this trend. Chargemaster, which renamed its public-facing operations BP Pulse when it was bought by the British multinational in 2018, lost £66.4m in 2024, while Shell EV Charging Solutions, the registered company behind Shell Recharge, lost £8.4m in the same year.

Chargepoint firms continue to bet that legislation mandating electric vehicles will eventually bring about profitability. But with 65% of all UK households having off-street parking, whatever customer base might materialise in the future will be far smaller than that which relies on petrol stations today.

Meanwhile, car companies are pivoting back to petrol following incomprehensible losses caused by a lack of EV uptake, while legislators are beginning to question if the electric-only world they dream of is possible in reality. Chargepoint operators must surely be asking themselves how long a game they can play and, if they build it, will they come?